Now, though, with oil demand grinding to a halt around the world as a result of the coronavirus response and WTI nudging $20 a barrel, many of those recently opened oil (and gas) wells are being shuttered.

That is bad news for the energy sector as a whole but may be good news before long for nat gas prices.

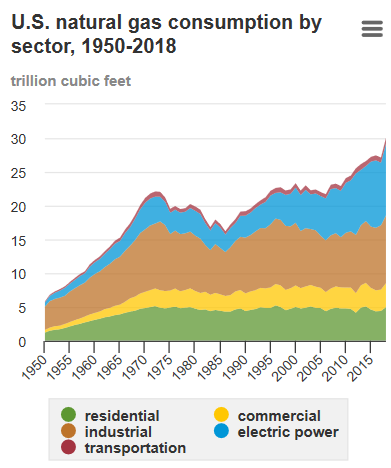

Nat gas demand isn’t comparable to that for oil. The primary use of oil is making gasoline, so as the world’s economies have shut down and driving has stopped, oil demand has been decimated. Over half of total demand for natural gas in the U.S., however, comes from electric power plants and home heating and cooling.

Increases there with everyone staying home should offset reductions elsewhere so, while there may be a small dip in demand, it won’t be that great. Oh, and U.S. total demand has been climbing for years…